|

|

| Home - Industry Article -

October 08 Issue |

Why Do Private Equity Firms Underachieve Their Planned ROI

|

By Gary Cokins, Global Product Marketing Manager, SAS Institute Inc.

Research studies reveal that only a minority of investments in

acquired companies achieve their targeted financial Return on Investment (ROI).

Explanations include poor strategy execution and inadequate marketing and sales

function tactics to grow sales profitably. Private equity firms are emerging as

significant players in the capital markets. They are increasingly deploying the

various improvement methodologies of enterprise performance management mounted

on an integrated enterprise information platform. Can integrating enterprise

performance management solutions resolve solve the underachieved ROI problem?

There is a sea change occurring in how the capital markets

allocate financial capital to organizations to fuel growth and prosperity.

Private equity funds and investment banks are displacing public capital markets

managed by international stock exchanges.1 Firms like these that invest in

acquisitions only, achieve their end-goal by raising the market value of their

acquired companies. Acquiring organizations are called capital market firms.

Their ultimate financial gain is realized from the buy-sell spread when they

divest each investment.

But there is a problem. Research studies reveal that only a minority achieve

their targeted financial return on investment (ROI). One study reported that

less than half of mergers achieve their goal.2 Why such poor results? Do they

over-plan, but under-execute their economic value creation activities?

Widespread adoption of the performance management framework may provide a

solution, but will the emergence of private equity funds accelerate the

application of performance management methodologies?3

In this article, I will initially describe a basic primer about capital markets

and what has created the growth in private equity firms. I will conclude with …

Who Are the Participants in Capital Markets?

In order to understand why private equity funds are sprouting globally, here is

a basic primer about capital markets.4 There are three capital markets that

profit-oriented organizations can tap to fuel their growth:

-

Public Capital Markets

These are the stock exchanges, such as the New York and London Stock Exchanges,

where individuals like you and I as well as investment managers of mutual and

pension funds and university endowments can invest along with others in publicly

traded companies. Investors will always bear some risk, but broad participation

by constant buyers and sellers typically moderates turbulence in stock price

changes. Stock exchanges are also where new companies raise funding through

initial public offerings (IPOs).

- Internal Capital Markets

This is where operating divisions within a parent company, such as Procter &

Gamble, are provided cash by senior executives at the parent’s headquarters. In

effect, divisions compete for the parent’s limited funding by submitting

proposals supported by justifications that estimate the financial returns they

can generate from the funds. In short, this is how financial resources are

allocated within a conglomerate.

- Private Capital Markets

This is the emerging player. You may recognize the four major types of

participants as angels (primarily individuals), venture capitalists (investors

betting on entrepreneurs), private equity funds and hedge funds. One

differentiator of private capital markets is they are not burdened by compliance

with government and public stock exchange regulations and laws.

From these descriptions, you can see that managers of private capital markets

are freer to identify investment opportunities and flexibly shift funds in those

directions. As a result, they can more quickly produce higher financial returns

than public and internal markets. Consequently, they are attracting insurance,

university endowment and retirement pension fund managers to supply them with

capital. Global liquidity available for investing is at record-high levels5 and

managers are chasing the highest risk-adjusted returns.

What Is Creating the Emergence of Private Equity Funds

The emergence of private equity funds is being stimulated by the governance

shortcomings of the other two types of capital markets.

Public capital markets will always be appealing to both investors and companies

seeking funding. This is partly because a substantial pool of global financial

savings is available, but more importantly, because investments are highly

liquid. That is, investors can easily enter and exit with their cash savings.

And this efficiency with pooled, risk-shared and liquid investments creates

broad diversification that translates into a minimal extra price premium to

purchase an equity position.

A shortcoming of public capital markets is that investment managers may behave

impatiently and be somewhat fickle in choosing which stocks to buy and sell.

Examples are the dot-com bust of 2000 and former US Federal Reserve Chairman

Alan Greenspan’s famous warning of ‘irrational exuberance.’ An impediment to

full attainment of profit potential is the legal separation of a company’s

ownership from its management. Investment managers rarely have access to

internal managerial information that the company’s managers have. Yet, at the

extreme, we observe young, recently minted MBAs at investment banking firms

pressuring and influencing accomplished executives to make decisions favoring

short-term financial results when relatively better decisions could result in

much higher long-term financial outcomes. Finally, because recent Enron-like

scandals have inspired regulatory burdens such as the Sarbanes-Oxley Act,

publicly owned companies incur significant out-of-pocket expenses for regulatory

compliance.

Internal capital markets can yield better financial performance because the

executive leadership has access to internal information, marketing plans, return

on investment analysis and projections. On the downside, however, similar to

public capital markets, internal capital markets also impede the ability to

attain full profit potential and maximize a company’s market value. But the

explanation is for a different reason: ‘Corporate socialism.’ What I mean by

this is that executives tend to patiently tolerate underperforming operating

divisions. Further, they may be reluctant to starve an old colleague heading a

division of his or her capital requests even though a sober and objective

assessment would recommend it. Politics and personal favoritism are present.

Strong divisions often subsidize weak ones.

In addition, executives tend to tolerate inefficiencies and waste that privately

owned companies would be more ruthless to address and remove. They tend to

universally apply standard performance measures that are not tailored to the

unique traits of a division’s industry. In short, some publicly owned company

executives are simply too slow at restructuring or divesting a division that is

not living up to its full potential.

Private Capital Markets Are Free of the Shortcomings of Public and Internal

Capital Markets

It is because private capital markets are not subject to the anchors and burdens

of public and capital markets that they are capable of relatively higher

performance. With a ‘Barbarians at the Gate’ reputation, private capital

managers reject internal capital allocation ‘socialism’ in unleashing higher

financial value from the tangible and intangible assets of their acquisitions.

Within the four types of private capital market participants, private equity

funds, such as the Blackstone Group and the Carlyle Group, are relatively more

aggressive than angels and venture capitalists. Private equity funds always have

an exit plan. In contrast, angels and venture capitalists are interested in

helping the young companies they are funding to successfully blossom as a

business, such as Yahoo! and Google

With this ‘buy low and sell high’ approach to investing, private equity funds

have one goal: To transform and turn around the acquired company. In other

words, the objective of a private equity firm can be summed up as follows: Buy a

pig (or some pigs) with other peoples’ money, spend a few years covering it with

lipstick and starving it so it has a more elegant figure and then sell the pig

at a profit to someone who thinks it is Miss Universe. The key to the process is

to be able to generate enough cash to pay for renting the ‘other peoples’ money’

while at the same time being able to afford all the lipstick. There is nothing

inherently evil in this process. The point is that the owners of a business

managed in such a way appear to have little concern for the business’ long-term

success or even its continued existence after it is sold. Their goal is to pay

for the interest and lipstick until they can sell the pig at a profit.

Performance Management aims at long-term sustained shareholder wealth creation.

Private equity funds do not necessarily acquire glamorous growth companies, but

often, older ones in mundane industries. Similar to a hospital patient in an

intensive care unit, companies acquired by private equity fund managers have one

purpose: To have their financial health improved and then be sold. However, the

stakes and risks are large. In contrast to public and internal capital markets,

with private equity funds, an investor’s capital is locked up until the sale of

the company – or until its parts are broken up and sold individually. There is a

price premium for an illiquid investment, which places additional pressure on

private equity fund managers to produce a high yield at the time of sale.

(Because these acquired companies upon exit are frequently purchased by publicly

owned companies, these assets are basically returned to the public capital

markets. The intensive care patient is returned to the traditional business

model.)

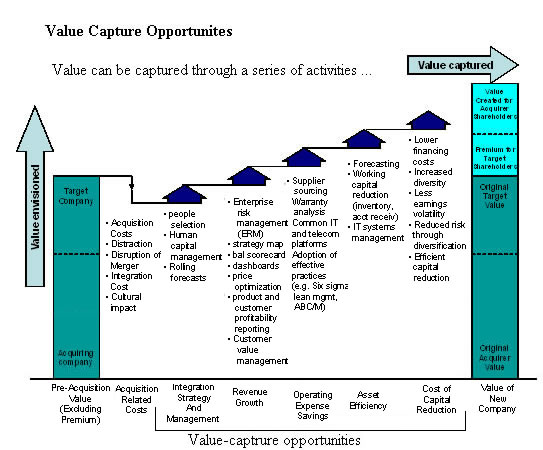

Five Value-Capture Action Categories to Realize Results

What actions do private equity funds take that produce incrementally higher

financial value in such short periods of time? The answer is simple. The

managers of the private equity funds do three things:

-

They hire talented senior executives to transform the acquired businesses.

- They have relatively higher performance targets and higher investment hurdle

rates.

- They equip these executives with the technology and tools that constitute and

support the Performance Management suite of methodologies.

The third item is where the private equities display their competence deploying

the power of business intelligence and performance management technologies. Both

the private equity managers and their hired guns who operate the businesses –

who have compensation reward packages tightly linked to improved financial and

non-financial performance goals – are adopting progressive managerial methods.

Realizing actual economic value from mergers and acquisitions (M&A) is a ‘high

stakes juggling act.’6 So many things must be correctly executed to maximize the

potential economic value. But problems arise such as the disruptions from

executive and employee turnover and from poor strategy execution – both the

modified business strategy and the M&A integration strategy.

Figure x displays five value-capture action categories that each contribute to

lifting shareholder value from an enterprise’s initial conditions. Although this

figure describes opportunities for an M&A deal, it can be applied to any

existing commercial organization.

Figure x: Value Capture Opportunities

Employees fear that the majority of the value lift will come from the third

arrow – operating expense savings – which is perceived as code for employee

layoffs. How can all five of the arrows generate the lift?

How Can Performance Management Methodologies Unlock Potential Value

There is confusion about what performance management (PM) at the enterprise

level is; and PM is too often narrowly described as just visual dashboard

measures and better financial reporting. It is much broader. PM is the

integration of multiple managerial methodologies (e.g., customer relationship

management, a balanced scorecard, Six Sigma) with an emphasis on analytics of

all flavors, and particularly risk management and predictive analytics. PM’s

methodologies themselves are not new; but organizations tend to independently

implement each of them sequentially, often using disconnected spreadsheet tools

rather than formal and proven information technologies. True PM deploys the

power of business intelligence (BI) to enable decision-making.

Although there are interdependencies of PM across all five value-capture

categories, different PM methodologies play a prominent role in each category:

-

Integration Strategy and Management

The heavy lifting is done in the next four categories to the right in Figure 1,

but in this first category the main PM methodology is human capital management (HCM).

Employees, like information, can be a powerful intangible asset to lift ROI. A

robust HCM system is not just an automated personnel database, but is much more

powerful in aiding employee selection and retention. For example, an

analytics-powered HCM system can quantify historical employee turnover and apply

statistical correlations from that history to the existing work force to

rank-order predict the most-to-least likely next employee to resign and

therefore enable management interventions. Both the employer and employee

benefit. With an aging work force approaching retirement at many companies, an

HCM system becomes essential.

- Revenue Growth

Several PM methodologies are engaged here:

-

Enterprise Risk Management (ERM)

ERM goes beyond just monitoring the traditional three pillars of market risk,

credit risk and operational risk. ERM also formally manages an organization’s

risk appetite with its risk exposure.

- Business Strategy Management and Execution David Norton, the co-author with

Professor Robert S. Kaplan of The Balanced Scorecard book series, has stated

that nine out of 10 companies fail to successfully implement their business

strategy.7 PM addresses this with the integration of:

- Strategy maps

- Scorecards (for strategic objectives and their associated key performance

indicators [KPIs] with targets)

- Dashboards (to cascade downward all measurements for operational actions

Incentives; and

- Analytics (to drill down to examine problem areas plus predict future outcomes).

-

Price Optimization

Pricing is too critical to be just a ‘thumb-in-the-air’ intuitive feel for what

price the market will bear. PM tools that optimize pricing include price

elasticity analysis of consumer demand. This is incorporated into scalable

forecasting and optimization routines that determine profit and volume

maximizing price-point for example for each retail stock keeping unit (SKU) at a

store specific level.

-

Product, Service-Line, Channel and Customer Profitability

Profit is calculated as sales minus costs, but few managerial accounting systems

properly trace and assign consumed resource expenses into costs; they rely on

antiquated broadly averaged cost allocations that distort true costs and

profits. Traditional costing practices mask and hide costs of a product or

service as a lump sum. PM’s inclusion of activity-based cost (ABC) principles

resolves these deficiencies. It is critical to have visibility and transparency

of the contributing elements of costs – with accuracy – and to understand the

many layers of profit margins.

-

Customer Value Management

To determine the value of a customer, marketing staffs have traditionally relied

on basic customer recency, frequency and monetary spend data (the RFM triad).

That data is not enough. Today, there is a much greater need for customer

intelligence that measures psycho-demographic information of customers as well

as to apply Customer Lifetime Value (CLV) metrics to answer the key questions,

‘What types of customer microsegments should we retain, grow, acquire and win

back? Which types should we not? How much should we spend with differentiated

deals or offers on each microsegment so we don’t risk over-spending on loyal

customers or under-spending on marginally loyal customers who may defect to a

competitor?’ The more powerful and scalable PM technologies answer these

questions and enable the ultimate microsegmentation – to the individual customer

or consumer.

Maximizing ROI is not accomplished by just growing sales, but rather by growing

sales ‘profitably.’ That is, ‘smart’ revenue growth rather than growth at any

cost.

- Operating Expense Savings

The recent popular improvement initiatives of Six Sigma and lean management help

the work force learn ‘how’ to think (and PM provides more reliable and useful

data for them, such as ABC information). But PM provides information for ‘where’

to think. PM brings focus. Improved productivity from business process

improvements will reduce expenses, but there are diminishing limits, and

breakthrough innovations stimulated by PM information will inevitably be

required. Warranty and service parts expenses are often loosely managed and PM

addresses these with analytics that quickly detect minor problems before they

escalate into major ones. PM also facilitates sourcing with supplier management

and consolidation tools.

- Asset Efficiency

For product-based companies, a large portion of their working capital is

inventory. PM’s solution to reduce inventories leverages statistically based

forecasts (updated periodically with demand history and potential influencing

factors) to reduce uncertainty so a company can more confidently match its

supply with demand. The objective is to minimize stockouts, shortages and

surplus unsold items. The resulting right-time and right-amount inventories

increase inventory turnover rates that in turn improve the financial gross

margin return on investment (GMROI).

For fixed assets, a growing portion of an organization’s expense structure is

its information technology expenses, and PM supports managing these

infrastructure expenses with IT value management reporting and planning systems

of technology capacity and usage as well as their associated workforce

requirements.

- Cost of Capital Reduction

The cost of capital has two components:

- The amount required and

- Its composite rate. PM methodologies contribute to reducing both.

PM’s ‘more with less’ productivity actions optimize the ‘amount’ of assets and

resources required to fulfill customer orders and meet strategic initiatives.

For banks this means better control of their capital reserves. PM provides risk

mitigation and reduced earnings volatility through powerful predictive analytics

to reduce the cost of capital ‘rate.’

Performance Management’s Bonus Methodology – Rolling Financial Forecasts

Capital market organizations hate surprises. PM cannot prevent surprises from

fraud, ethics violations or unexpected financial re-statements (but PM’s

analytics can provide earlier warnings). A surprise that PM can reduce for

capital market firms is an earlier alert that their acquired company will ‘miss

their numbers.’ Today, the annual budget is arguably outdated as a financial

control instrument in part because it is obsolete soon after being published.

But worse, the annual budget is criticized for not effectively allocating

resources to their highest returns. PM addresses these shortcomings by shifting

the accountants’ mentality from negotiating the next fiscal year’s incremental

percent spending changes with managers to a more logical approach. This approach

models resource capacity planning, staffing levels and supplier spending.

Imagine producing a budget twelve times a year. That is a nightmare for the

accountants. Budgets are financial translations of non-financial operations. PM

tools combine future volume-based demand drivers (e. g. sales projections) with

funding for strategic initiatives. Since sales forecasts are constantly updated

and because a strategy is dynamic, not static, then with constant adjustments

various PM methodologies automate the translation of operations into rolling

financial forecasts.

What Leads to the Unfulfilled Promises of ROI for Capital Market Firms

To be clear, the boards of directors of companies listed in public capital

markets are not ignoring performance management. They are making the transition

from a pre-Enron ceremonial role to a new era of activist boards that more

seriously accept their corporate governance responsibilities to represent

shareholders.

Capital market firms place high importance on executive leadership. And they

should. From reading this article, you may conclude that the performance

management methodologies are like cog gears, and the executives with the

best-in-class technologies that support PM’s methodologies can just push or pull

the levers and pulleys and watch the dials. To achieve superior results,

executive leaders must exhibit vision and inspiration. That is what a work force

responds to.

However, to fully achieve the highest potential in the right side of Figure 1 –

Value of New Company – an enterprise cannot rely on a rudder-and-stick to get

there. The executive team and their work force need integrated business

intelligence and performance management software for those gears to mesh and

revolve at faster speeds. The premier software technology not only integrates

PM’s suite of methodologies, but its underlying architecture is on a common data

platform and its compute power is optimized for analytics – particularly

predictive analytics. The result and benefit is better, faster, cheaper – and

smarter.

Today, a building contractor would never manually excavate a foundation with

shovels; they equip their employees with industrial-strength power tools. The

same goes for most companies – at least those aware of the shortcomings of

spreadsheets and other nonintegrated information systems that are limited in

supporting control, analysis and decision-making.

Enterprise resource planning (ERP) software is helping companies get operational

control, but ERP software is not designed to transform transactional data into

information needed for decision support. As the capital market firms influence

(or demand) their acquired companies to adopt and integrate PM methodologies

with their supporting technology, their desired ROI targets will be achieved and

possibly surpassed.

1 In 2006, private equity funds accounted for 35 percent of global acquisitions,

which was double the prior 10-year average of 17 percent (PricewaterhouseCoopers

study).

2 Deloitte Research – Economist Unit M&A Survey (2007).

3 To learn the basics about the performance management framework, read “The

Tipping Point for Performance Management” at http://www.dmreview.com/article_sub.cfm?articleId=1027292.

4 For more information, Google Professor Jayanth R. Varma, Indian Institute of

Management, Ahmedabad, India, who inspired this article.

5 see http://usmarket.seekingalpha.com/article/22629

6 “Mergers and Acquisitions: What CFOs Should Consider Asking Before the Deal is

Done;” March 18, 2008 webinar; Carol Bailey and Trevear Thomas, Deloitte

Consulting LLP.

7 David Norton, co-author of “The Balanced Scorecard: Translating Strategy into

Action” at the Balanced Scorecard Collaborative Summit on November 7, 2006.

Gary Cokins, CPIM, is Global Product Marketing Manager of

Performance Management Solutions with SAS. He is an internationally recognized

expert, speaker and author in advanced cost management and performance

improvement systems. After earning an Industrial Engineering degree from Cornell

University in 1971 and an MBA from Northwestern University Kellogg Graduate

School of Management, Gary began his career as a Financial Controller and

Operations Manager with FMC Corp. He worked 15 years as a Consultant at

Deloitte, KPMG Peat Marwick and Electronic Data Systems (EDS), where he headed

EDS’ Cost Management Consulting Services. Gary was the lead author of the

acclaimed “An ABC Manager’s Primer” sponsored by the Institute of Management

Accountants (IMA). His “Activity-Based Cost Management: An Executive’s Guide”

recently ranked as the best-selling book of 151 titles on the topic. Gary’s

other books include “Activity-Based Cost Management: Making it Work,”

“Activity-Based Cost Management in Government”, and his latest work,

“Performance Management: Finding the Missing Pieces to Close the Intelligence

Gap.” He has served on committees of professional societies including CAM-I,

AICPA, the Supply Chain Council, the American Society for Quality (ASQ) and the

Institute of Management Accountants (IMA). Gary is a member of the editorial

advisory board of the Journal of Cost Management. He is an Instructor for the

IMA, the Institute of Industrial Engineers (IIE), and the Purchasing Management

Association of Canada (PMAC). For article feedback, contact Gary at

gary.cokins@sas.com

|

|

|